Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

The Housing Market Faces Two Big Issues

The housing market faces two big issues right now. The biggest challenge is how few homes there are for sale. Mark Fleming, Chief Economist at First American, explains the root causes of today’s low supply:

“Two dynamics are keeping existing-home inventory historically low – rate-locked existing homeowners and the fear of not finding something to buy.”

Let’s break down these two big issues in today’s housing market.

Rate-Locked Homeowners

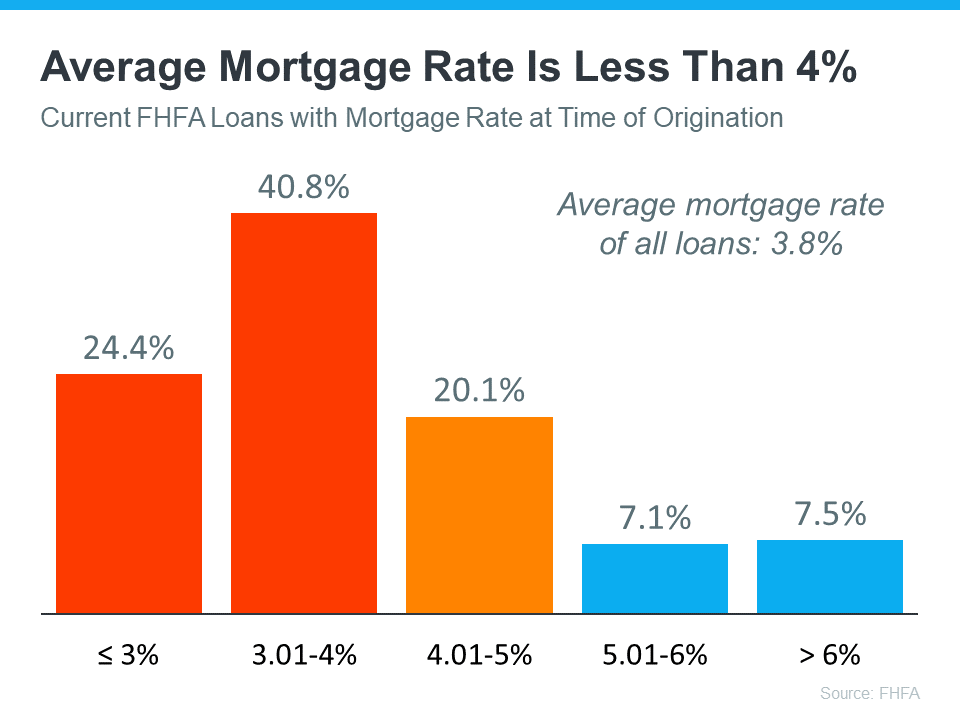

According to the Federal Housing Finance Agency (FHFA), the average interest rate for current homeowners with mortgages is less than 4% (see graph below):

Today, the typical mortgage rate offered to buyers is over 6%. As a result, homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as being rate locked.

When so many homeowners are rate locked and reluctant to sell, it’s a challenge for a housing market that needs more inventory. However, experts project mortgage rates will gradually fall this year, and that could mean more people will be willing to move.

The Fear of Not Finding Something To Buy

The other factor holding back potential sellers is the fear of not finding another home to buy. People are on the sidelines as they wait for more homes to come to the market. That’s why, if you’re on the fence about selling, it’s important to consider all your options. That includes newly built homes, especially right now when builders are offering concessions like mortgage rate buydowns.

What Does This Mean for You?

These two issues are keeping the supply of homes for sale lower than pre-pandemic levels. But if you want to sell your house, today’s market is a sweet spot that can work to your advantage.

Be sure to work with a local real estate professional to explore the options you have right now, which could include leveraging your current home equity. According to ATTOM:

“. . . 48 percent of mortgaged residential properties in the United States were considered equity-rich in the fourth quarter, meaning that the combined estimated amount of loan balances secured by those properties was no more than 50 percent of their estimated market values.”

This could make a major difference when you move. Work with a local real estate expert to learn how putting your equity to work can keep the cost of your next home down.

Bottom Line

Rate-locked homeowners and the fear of not finding something to buy are keeping housing inventory low across the country. As mortgage rates start to come down this year and homeowners explore all their options, we should expect more homes to come to the market.

Pre-Approval in 2023: What You Need To Know

One of the first steps in your homebuying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains:

“In a preapproval [sic], the lender tells you which types of loans you may be eligible to take out, how much you may be approved to borrow, and what your rate could be.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand your options and what you may be able to borrow.

How does it work? As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

Another added benefit is pre-approval can help a seller feel more confident in your offer because it shows you’re serious about buying their house. A recent article from Forbes notes:

“From the seller’s perspective, a preapproval [sic] letter from a reputable local lender often can make the difference between accepting and rejecting an offer.”

This goes to show, even though you may not face the intense bidding wars you saw if you tried to buy during the pandemic, pre-approval is still an important part of making a strong offer. In fact, Christy Bieber, Personal Finance Writer at The Motley Fool explains it may be the most important part of making an offer:

“Pre-approval maximizes the chances you’ll be able to actually close the deal – and sellers want to see that.

The fact that a pre-approval gives you a better chance of getting your offer accepted is undoubtedly the most important reason to complete this step . . .”

Bottom Line

Getting pre-approved is an important first step towards buying a home. It lets you know what you can borrow and shows sellers you’re serious about purchasing their home. What’s your next real estate goal? I’d be honored to help. (614) 674-3939

Understand These Important Terms

Buying a home is a major transaction that can seem even more complex when you don’t understand these important terms used throughout the process.

If you’re not comfortable asking your sales agent questions as they arise, find a new one! A professional embraces the fiduciary trust you place with them. You should ALWAYS feel confident and empowered.

VA Loans Can Help Veterans Achieve Their Dream of Homeownership

For over 78 years, Veterans Affairs (VA) home loans have provided millions of veterans with the opportunity to purchase homes of their own. If you or a loved one have served, it’s important to understand this program and its benefits.

Here are some things you should know about VA loans before you start the homebuying process.

What Are VA Loans?

VA home loans provide a pathway to homeownership for those who have served our nation. The U.S. Department of Veterans Affairs describes the program like this:

“VA helps Servicemembers, Veterans, and eligible surviving spouses become homeowners. As part of our mission to serve you, we provide a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.”

Top Benefits of the VA Home Loan Program

In addition to helping eligible buyers achieve their homeownership dreams, VA loans have several other great benefits for buyers who qualify. According to the Department of Veteran Affairs:

- Qualified borrowers can often purchase a home with no down payment.

- Many other loans with down payments under 20% require Private Mortgage Insurance (PMI). VA Loans do not require PMI, which means veterans can save on their monthly housing costs.

- VA-Backed Loans often offer competitive terms and mortgage interest rates.

A recent article from Veterans United sums up just how impactful this loan option can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

John Bell, Acting Executive Director of the Department of Veterans Affairs Loan Guaranty Service, also explains why this program is so powerful:

“It provides early ownership for many people that would not have that opportunity to begin with. Since there’s no down payment, it allows people to hold their wealth and it gives them the ability to have long term financial security by being able to own a house and let that equity grow.”

Bottom Line

Homeownership is the American Dream. Our veterans sacrifice so much in service of our nation, and one way we can honor and thank them is to ensure they have the best information about the benefits of VA home loans. Thank you for your service.

For more information about loans, visit “Buying” on my website.

Saving for a Down Payment? Here’s What You Need To Know.

As you set out to buy a home, saving for a down payment is likely top of mind. But you may still have questions about the process, including how much to save and where to start.

If that sounds like you, your down payment could be more in reach than you originally thought. Here’s why.

The 20% Down Payment Myth

If you believe you have to put 20% down on a home, you may have based your goal on a common misconception. Freddie Mac explains:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Unless it’s specified by your loan type or lender, it’s typically not required to put 20% down. According to the latest Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. There are even loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

This is good news for you because it means you could be closer to your homebuying dream than you realize. For more information, turn to a trusted lender.

Down Payment Assistance Programs Can Be a Game Changer

A professional will be able to show you other options that could help you get closer to your down payment goal. According to latest Homeownership Program Index from downpaymentresource.com, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments.

A recent article explains why programs like these are helpful:

“These resources can immediately build your home buying power and help you take action sooner than you thought possible.”

And if you’re wondering if you have to be a first-time buyer to qualify for these programs, that’s not always the case. According to an article from downpaymentresource.com:

“It is a common misconception that homebuyer assistance is only available to first-time homebuyers, however, 38% of homebuyer assistance programs in Q1 2022 did not have a first-time homebuyer requirement.”

There are also location and profession-based programs you could qualify for as well.

Bottom Line

Saving for your down payment is an important first step on your homebuying journey. Connect with a local real estate advisor and trusted lender today to begin exploring your options.