Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Pre-Approval in 2023: What You Need To Know

One of the first steps in your homebuying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains:

“In a preapproval [sic], the lender tells you which types of loans you may be eligible to take out, how much you may be approved to borrow, and what your rate could be.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand your options and what you may be able to borrow.

How does it work? As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

Another added benefit is pre-approval can help a seller feel more confident in your offer because it shows you’re serious about buying their house. A recent article from Forbes notes:

“From the seller’s perspective, a preapproval [sic] letter from a reputable local lender often can make the difference between accepting and rejecting an offer.”

This goes to show, even though you may not face the intense bidding wars you saw if you tried to buy during the pandemic, pre-approval is still an important part of making a strong offer. In fact, Christy Bieber, Personal Finance Writer at The Motley Fool explains it may be the most important part of making an offer:

“Pre-approval maximizes the chances you’ll be able to actually close the deal – and sellers want to see that.

The fact that a pre-approval gives you a better chance of getting your offer accepted is undoubtedly the most important reason to complete this step . . .”

Bottom Line

Getting pre-approved is an important first step towards buying a home. It lets you know what you can borrow and shows sellers you’re serious about purchasing their home. What’s your next real estate goal? I’d be honored to help. (614) 674-3939

Understand These Important Terms

Buying a home is a major transaction that can seem even more complex when you don’t understand these important terms used throughout the process.

If you’re not comfortable asking your sales agent questions as they arise, find a new one! A professional embraces the fiduciary trust you place with them. You should ALWAYS feel confident and empowered.

Home Equity, The Truth About Negative Headlines

Home equity has been a hot topic in real estate news lately. You may have heard there’s a growing number of homeowners with negative equity. Don’t let those headlines scare you.

In truth, the headlines don’t give you all the information you really need to understand what’s happening and at what scale. Let’s break down one of the big equity stories you may be seeing in the news, and what’s actually taking place. That way, you’ll have the context you need to understand the big picture.

Headlines Focus on Short-Term Home Equity Numbers and Fail To Convey the Long-Term View

One piece of news circulating focuses on the percentage of homes purchased in 2022 that are currently underwater. The term underwater refers to a scenario where the homeowner owes more on the loan than the house is worth. This was a huge issue when the housing market crashed in 2008, but it much less significant today.

Media coverage right now is based loosely on a report from Black Knight, Inc. The actual report from that source says this:

“Of all homes purchased with a mortgage in 2022, 8% are now at least marginally underwater and nearly 40% have less than 10% equity stakes in their home, . . .”

Let’s unpack that for a moment and provide the bigger picture. The data-bound report from Black Knight is talking specifically about homes purchased in 2022, but media headlines don’t always mention that timeframe or provide the surrounding context about how unusual of a year 2022 was for the housing market. In 2022, home price appreciation soared, and it reached its max around March-April. Since then, the rate of appreciation has been slowing down.

Homeowners who bought their house last year right at the peak or those who paid more than market value in the months that followed are more likely to fall into the category of being marginally underwater. The qualifier marginally is another key piece of the puzzle the media isn’t necessarily including in their coverage.

So, what does that mean for those who purchased a home in 2022? It’s important to remember, owning a home is a long-term investment, not a short-term play. When headlines focus on the short-term view, they’re not necessarily providing the full context.

Typically speaking, the longer you stay in your home, the more equity you gain as you pay down your loan and as home prices appreciate. With recent market conditions, you may not have gained significant equity right away if you owned the home for just a few months. But it’s also true that many homeowners who recently bought their house are unlikely to be looking to sell quite yet.

Bottom Line

As with everything, knowing the context is important. Be informed and be empowered. If you have questions about real estate headlines or about how much equity you have in your home, call me. (614) 674-3939

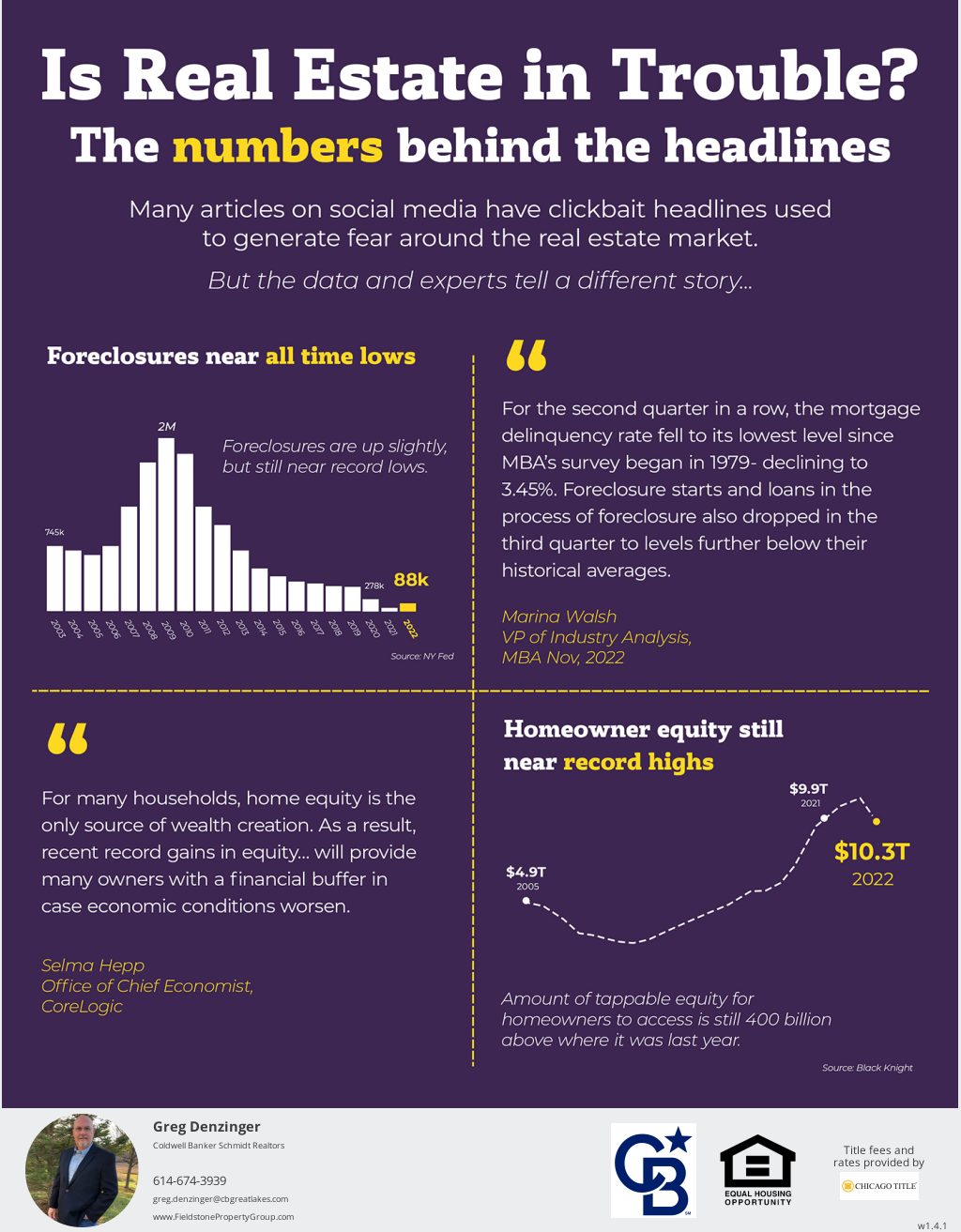

Truth or Clickbait

Some headlines out there intentionally paint today’s real estate market as doom-and-gloom – but when you take a step back you can see the historical data tells a different story. Take a look at the complete picture of where we are in regard to Homeowner Equity, Foreclosures, and Inventory.

What’s Going on with Home Prices? Get Local Advice.

If you’re thinking about buying or selling a home this year, you may have questions about what’s happening with home prices today as the market cools. In the simplest sense, nationally, experts don’t expect prices to come crashing down, but the level of home price moderation will depend on factors like supply and demand in each local market.

That means, moving forward, home price appreciation will continue to vary by location, with more significant changes happening in overheated areas. Here’s a quick snapshot of what the experts are saying:

Danielle Hale, Chief Economist at realtor.com, says:

“The major question on the minds of homeowners and aspiring buyers alike is what will happen to home prices. . . Soaring prices were propelled by all-time low mortgage rates which are a thing of the past. As a result, home price growth is expected to continue slowing, dipping below its pre-pandemic average to 5.4% for 2023, as a whole.”

Mark Fleming, Chief Economist at First American, says:

“House price appreciation has slowed in all 50 markets we track, but the deceleration is generally more dramatic in areas that experienced the strongest peak appreciation rates.”

Taylor Marr, Deputy Chief Economist at Redfin, says:

“For those bearish folks eagerly awaiting the home price crash, you’ll have to keep waiting. As much as demand is pulling back supply is as well reducing downward pressure on prices in the short run.”

John Paulson, Founder of Paulson & Co., says:

“It’s true – housing may be a little frothy. So housing prices may come down or they may plateau . . .”

What Does This Mean for You?

The best way to get the answers you need is to lean on a local real estate advisor. We’re happy to explain the latest trends in our market so you can make a confident and informed decision on your next step toward buying or selling a home.

Bottom Line

If you have questions about what’s happening with home prices today, let’s connect. You may also find the local market data I’ve compiled helpful.

VA Loans Can Help Veterans Achieve Their Dream of Homeownership

For over 78 years, Veterans Affairs (VA) home loans have provided millions of veterans with the opportunity to purchase homes of their own. If you or a loved one have served, it’s important to understand this program and its benefits.

Here are some things you should know about VA loans before you start the homebuying process.

What Are VA Loans?

VA home loans provide a pathway to homeownership for those who have served our nation. The U.S. Department of Veterans Affairs describes the program like this:

“VA helps Servicemembers, Veterans, and eligible surviving spouses become homeowners. As part of our mission to serve you, we provide a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.”

Top Benefits of the VA Home Loan Program

In addition to helping eligible buyers achieve their homeownership dreams, VA loans have several other great benefits for buyers who qualify. According to the Department of Veteran Affairs:

- Qualified borrowers can often purchase a home with no down payment.

- Many other loans with down payments under 20% require Private Mortgage Insurance (PMI). VA Loans do not require PMI, which means veterans can save on their monthly housing costs.

- VA-Backed Loans often offer competitive terms and mortgage interest rates.

A recent article from Veterans United sums up just how impactful this loan option can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

John Bell, Acting Executive Director of the Department of Veterans Affairs Loan Guaranty Service, also explains why this program is so powerful:

“It provides early ownership for many people that would not have that opportunity to begin with. Since there’s no down payment, it allows people to hold their wealth and it gives them the ability to have long term financial security by being able to own a house and let that equity grow.”

Bottom Line

Homeownership is the American Dream. Our veterans sacrifice so much in service of our nation, and one way we can honor and thank them is to ensure they have the best information about the benefits of VA home loans. Thank you for your service.

For more information about loans, visit “Buying” on my website.

The Emotional and Non-financial Benefits of Homeownership

With higher mortgage rates, you might be wondering if now’s the best time to buy a home. While the financial aspects are important to consider, there are also powerful non-financial reasons it may make sense to make a move. Here are just a few of the benefits that come with homeownership.

Homeowners Can Make Their Home Truly Their Own

Owning your home gives you a significant sense of accomplishment because it’s a space you can customize to your heart’s desire. That can bring you added happiness.

In fact, a report from the National Association of Realtors (NAR) shows making updates or remodeling your home can help you feel more at ease and comfortable in your living space. NAR measures this with a Joy Score that indicates how much happiness specific home upgrades bring. According to NAR:

“There were numerous interior projects that received a perfect Joy Score of 10: paint entire interior of home, paint one room of home, add a new home office, hardwood flooring refinish, new wood flooring, closet renovation, insulation upgrade, and attic conversion to living area.”

And as a homeowner, unless there are specific homeowner’s association requirements, you typically won’t have to worry about the changes you can and can’t make.

If you rent, you may not have the same freedom. And if you do make changes as a renter, there’s a good chance you’ll need to revert them back at the end of your lease based on your rental agreement. That can add additional costs when you move out.

The Responsibilities of Homeownership Give You a Greater Sense of Achievement

There’s no denying taking care of your home is a large responsibility, but it’s one you’ll take pride in as a homeowner. Freddie Mac explains:

“As the homeowner, you have the freedom to adopt a pet, paint the walls any color you choose, renovate your kitchen, and more. . . . Of course, along with the freedoms of homeownership come responsibilities, such as making your monthly mortgage payments on time and maintaining your home. But as the property owner, you’ll be caring for your own investment.”

You’re not taking care of a living space that belongs to someone else. The space is yours. As an added benefit, you may get a return on investment for any upgrades or repairs you make.

Homeownership Can Lead to Greater Community Engagement

That sense of ownership and your feelings of responsibility can even extend beyond the walls of your home. Your home also gives you a stake in your community. Because the average homeowner stays in their home for longer than just a few years, that can lead to having a stronger connection to your local area. NAR notes how that can benefit you:

“Living in one place for a longer amount of time creates an obvious sense of community pride, which may lead to more investment in said community.”

If you’re looking to put down roots, homeownership can help fuel a sense of connection to the area and those around you.

Bottom Line

Is someone you know planning to buy a home? There are incredible benefits waiting at the end of the journey, including the ability to customize your home, the sense of achievement homeownership brings, and a greater connection to your community. Call me today. I’d be honored to start you on the path that’s right for you.

Saving for a Down Payment? Here’s What You Need To Know.

As you set out to buy a home, saving for a down payment is likely top of mind. But you may still have questions about the process, including how much to save and where to start.

If that sounds like you, your down payment could be more in reach than you originally thought. Here’s why.

The 20% Down Payment Myth

If you believe you have to put 20% down on a home, you may have based your goal on a common misconception. Freddie Mac explains:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Unless it’s specified by your loan type or lender, it’s typically not required to put 20% down. According to the latest Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. There are even loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

This is good news for you because it means you could be closer to your homebuying dream than you realize. For more information, turn to a trusted lender.

Down Payment Assistance Programs Can Be a Game Changer

A professional will be able to show you other options that could help you get closer to your down payment goal. According to latest Homeownership Program Index from downpaymentresource.com, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments.

A recent article explains why programs like these are helpful:

“These resources can immediately build your home buying power and help you take action sooner than you thought possible.”

And if you’re wondering if you have to be a first-time buyer to qualify for these programs, that’s not always the case. According to an article from downpaymentresource.com:

“It is a common misconception that homebuyer assistance is only available to first-time homebuyers, however, 38% of homebuyer assistance programs in Q1 2022 did not have a first-time homebuyer requirement.”

There are also location and profession-based programs you could qualify for as well.

Bottom Line

Saving for your down payment is an important first step on your homebuying journey. Connect with a local real estate advisor and trusted lender today to begin exploring your options.